With the current concerns surrounding the CoronaVirus global equity, fixed income, credit and commodity markets the question we have is how rapidly are markets re-pricing risk assets and will this be another opportunity to sell volatility?

In a two-part commentary, we will review the VIX Listed Options Market and the CBOE’s Put and Call Index.

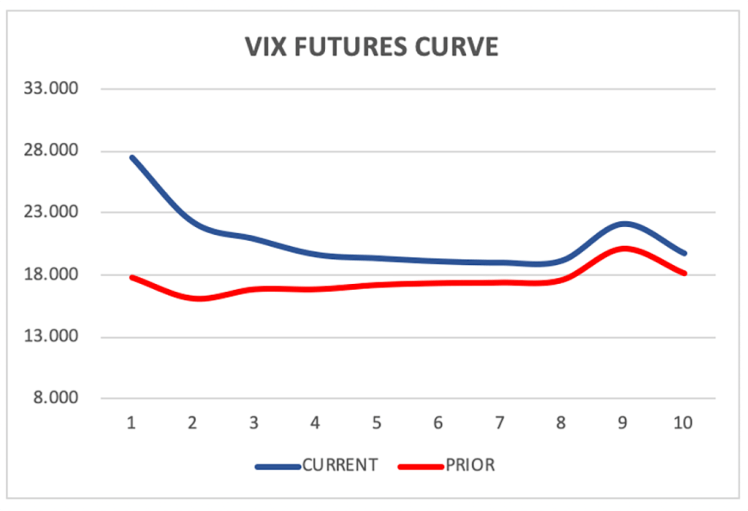

So to the VIX Options. Taking a snapshot view of the VIX futures pricing over the last few days shows a sharp move in the front end of the curve supported by a parallel move up, with the curve now in backwardation we’d expect to see significant pressure on the front end in the coming days.

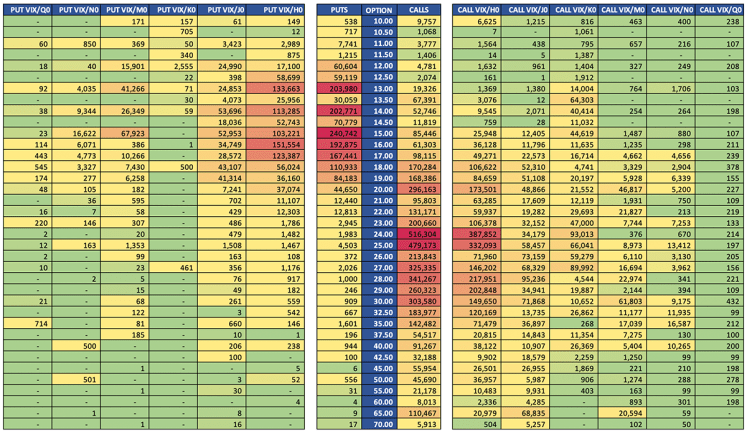

Our proprietary heat map of listed VIX Options shows there are significant concentrations are in the one-month maturity. Upside risk has pronounced concentrations at the 24 and 25 strike calls while it is the 13, 14 and 15 strike puts that appear to anchor the downside normalisation.

We hope you find this helpful.