Mark your calendars! There’s only one week to go before International Bestselling, Author Jack Schwager’s latest book, “Unknown Market Wizards” hits the market.

Learn from exceptionally successful traders and how they achieved extraordinary results. Jack Schwager takes us to a world of trading wisdom and insights, with a touch of humour including revelations about the human side of trading.

“Unknown Market Wizards” is published by Harriman House Books and we are excited to be a partner for the launch!

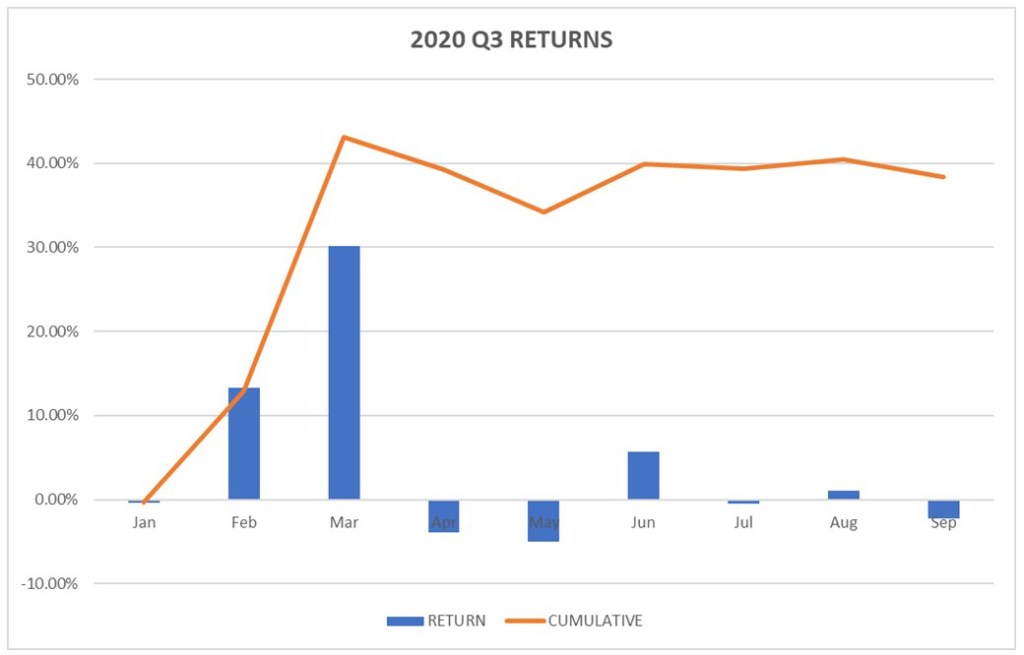

We are pleased to announce our Private Company Trading Results.

Our business generated a 38.31% return for the first nine months of 2020 on our capital base.

Q1 was dominated by the global spread of the COVID19 virus and the concurrent economic shutdowns. For markets, this resulted in a massive re-pricing of risk assets with commodity, equity and fixed income volatility reaching all-time highs as spot markets dropped and even safe-haven assets declined as investors sought liquidity.

Q2 brought a bifurcation between markets and the economy. The start of an equity market rally centred around technology stocks and massive fiscal support programmes counter-balanced the re-structuring / bankruptcies across airlines, hotels and retail sectors. The Russia-Saudi oil price war intensified and as structural flaws in certain retail derivatives became apparent this helped to drive WTI futures into negative territory.

Q3 confirmed the US Federal Reserve would move to use average inflation targeting and imbed a narrative of “lower for a lot longer”, while Central Banks globally continue to ask policymakers to deploy more fiscal resources into the economy.

Looking forward to Q4 risk and derivative markets are pricing material volatility as we see both a stalled negotiation on the US fiscal stimulus and a potentially contested US election. Central Bankers globally continue to urge authorities to deploy more fiscal resources we see two principal, and frustratingly opposing, risks ahead; the deflation and the inflation narratives.

As we move forward into Q4 we reiterate our trading stance. The risk factors we are watching carefully for signs of change are fiscal support measures, monetary stimulus, consumer spending and money flows into financial assets. Derivative markets are pricing material risk in the near term and while forward earnings and dividend distributions have moved up we are cautious and look across the economy for the persistence of material re-structuring & bankruptcies (retail, airlines, cinemas) and dislocations in parts of the credit markets as they adjust to the new consumer and corporate behaviours.

As always we’d like to thank our trading execution partners from Interactive Brokers and Saxo Bank. Thank you to both Chatham House and Geopolitical Futures their perspectives.

Re-affirming our social commitment we continue with our 2020 donation programme to include Feeding Hong Kong and Hong Kong’s Save The Children Coronavirus Relief Fund.

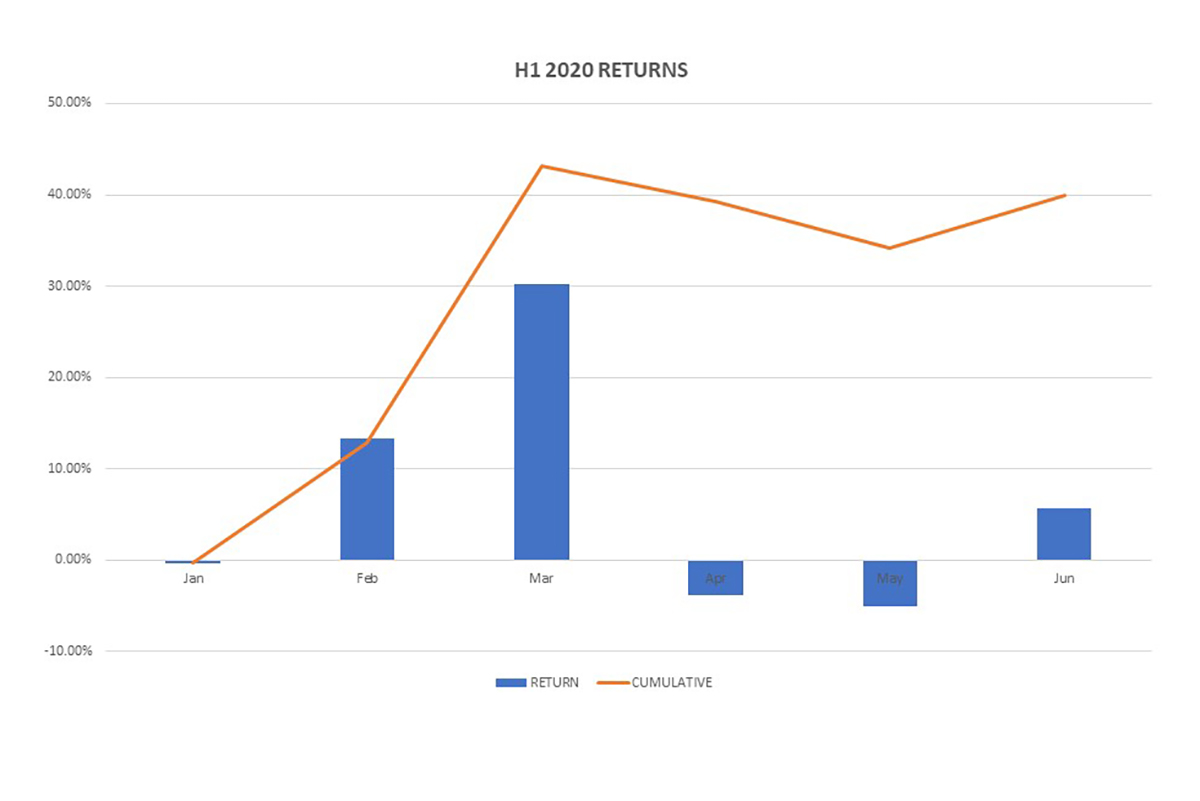

We are pleased to announce our Private Company First Half Trading Results.

Our business generated a 39.91% return for the first half of 2020 on our capital base.

We started the year with a cross-asset net long volatility exposure. Our portfolio was positioned around Gold, US Shale Pipeline Equities and US Interest Rates. Despite the market making new highs in January, we had concerns with the continued melt-up in equities, as we were reaching and exceeding key valuation metrics, while volatility measures in these asset classes registered near all-time lows.

As the financial impact of the COVID-19 pandemic became apparent in early February we expanded our portfolio risk to incorporate S&P500, Nasdaq and Russell2000 and GBP/USD volatility structures. During April and until mid-May we opted for a cautious risk stance, in part due to unwinding into the high volatility levels and not encouraged by binary risk profile presented by Fiscal Support Measures & Monetary Stimulus relative to Economic shutdowns and the growing COVID19 Health Crisis.

Mid-May we acknowledged that the reaction function of the markets to the fiscal support and monetary stimulus was deeply positive. Adjusting our existing strategy to acquire short-dated volatility in assets that had multi-time zone liquidity allowed us to take advantage of several market factors trading across time-zones.

As we move forward risk factors we are watching carefully for signs of change are fiscal support measures, monetary stimulus, consumer spending and money flows in financial assets. Derivative markets have re-priced forward earnings and dividend distributions, however we are looking across the economy for the persistence of material bankruptcies and dislocations in parts of the credit markets to adjust consumer and corporate behaviour.

As always we’d like to thank our trading execution partners from Interactive Brokers and Saxo Bank. Thanks to Chatham House and Geopolitical Futures their perspectives.

Re-affirming our social commitment we continue with our 2020 donation programme to include Feeding Hong Kong and Hong Kong’s Save The Children Coronavirus Relief Fund.